SECTION 1: APPLICANT INFORMATION

Applicant Name: dominic

Project Name: MYSO Finance

Project Description: MYSO Finance is a DeFi lending protocol specialized in customizable loans and covered calls for nearly any token.

Team Members and Roles:

- Aetienne, Founder & Developer

- Jamie, Lead Full Stack Developer

- Mykola, Senior Full Stack Developer

- Denis, Growth and Research

- Dominic, Operations and Partnerships

| Project Links: | |

|---|---|

| - | Website: https://www.myso.finance/ |

| - | dApp: https://app.myso.finance/ |

| - | Docs: Introduction | MYSO Docs |

| - | Medium: https://medium.com/mysofinance |

| - | X: https://twitter.com/MysoFinance |

| - | Github: GitHub - mysofinance/v2 |

Contact Information

Point of Contact: @domvnz

Point of Contact’s TG handle: @domvnz

Twitter: @domvnz

Email: dominic@myso.finance

Do you acknowledge that your team will be subject to a KYC requirement?: Yes

SECTION 2a: Team and Product Information

Team experience:

The five team members come from a varied background in finance and engineering, with several years of professional experience in crypto. We have a deep understanding of both DeFi and TradFi, particularly financial derivatives.

Aetienne, Founder & Developer: Before founding MYSO Finance, Aetienne worked as an Innovation Manager in Swisscom’s FinTech Team and served as Blockchain Technical Lead and Financial Engineer at Bank Vontobel. He has been awarded finalist at several hackathons, including ETHOnline and HackMoney, and is passionate about building new DeFi primitives and developing innovative financial products. He holds two Master’s degrees in Finance and Business Informatics, as well as a Bachelor’s in Industrial Engineering.

Jamie, Lead Full Stack Developer: Before joining MYSO Finance in early 2022, Jamie worked as a Mechanical Engineer and Data Analyst/programmer for USNR. He founded JKP Applications in early 2020, which develops software and data solutions, and has worked with multiple projects in both web2 and web3 spaces. He has been awarded finalist at starknet hackathon, EthGlobal HackFS, gitcoin GR10, Iotex India hackathon 2021, and others and was a founding member of dCompass, a recipient of filecoin and gitcoin grants. He holds two Master’s degrees in aerospace engineering and applied mathematics.

Dominic, Operations and Partnerships: Before joining MYSO, Dominic served as a FinTech Innovation Manager at Swisscom, where he played a key role in driving innovation and developing new digital products. Prior to this, he worked as an Investment Analyst at a private equity FinTech fund, and as Wealth Management Advisor for single family offices at Credit Suisse. He is a Chartered Financial Analyst (CFA) Charterholder and holds a Bachelor’s degree in Banking and Finance.

What novelty or innovation does your product bring to Arbitrum?

MYSO combines primitives from structured products with DeFi lending, i.e., all loans on MYSO are structured as trustless ‘covered calls.’ This opens up numerous use cases such as:

-

Bespoke Loans: MYSO enables protocols (and anyone else) to create fully customizable peer-to-peer lending markets for nearly any token. For DAOs, MYSO is a powerful new tool to increase the utility of their native token and to enable them to use their token reserves in a more productive and strategic way. Moreover, MYSO also allows DAOs to create highly customizable loan requests and collectively fund these debt venture deals. Thanks to the embedded conversion feature (similar to convertible bonds in TradFi), DAOs/borrowers can reduce their overall stablecoin borrowing costs while giving lenders upside participation in their native token.

-

Covered Calls: MYSO enables bespoke and fully customizable covered calls without counterparty risk for nearly any token. The offering allows token holders to lend otherwise idle tokens to generate upfront stablecoin revenue by writing call options.

Moreover, the protocol comes with several advanced features such as native one-click looping support, advanced collateral management, and many more that make the protocol truly a category leader.

Is your project composable with other projects on Arbitrum? If so, please explain:

Yes, for example, MYSO has already been integrated on Arbitrum with Gains Network and Mozaic Finance, allowing these protocols to establish customized lending markets tailored to their respective communities. MYSO has been built with easy integratability in mind, allowing for any kind of ERC20 to be used for lending and borrowing (including Rebasing tokens), as well as handling more complex reward-accruing tokens such as GLP from GMX. Additionally, given MYSO’s oracle independence, we can integrate lending markets for tokens where oracle support might not (yet) be available. Furthermore, our protocol has already been used by several treasuries for yield enhancement using our trustless covered call offering, and we’d be keen to further grow this in the Arbitrum ecosystem.

Do you have any comparable protocols within the Arbitrum ecosystem or other blockchains?

Thetanuts, Timeswap, Vendor

How do you measure and think about retention internally?

We track returning users and user stickiness using Google Analytics and other tools (see attached screenshots). Moreover, we also monitor several other key metrics that reflect user engagement and interaction on each chain. This includes the total volume of loans, the number of loans, the number of active loans, vaults created, and the number of loan offers per user. Alongside these metrics, we also engage with users through feedback surveys to improve retention and user experience.

Relevant usage metrics - Please refer to the OBL relevant metrics chart . For your category (DEX, lending, gaming, etc) please provide a list of all respective metrics as well as all metrics in the general section:

General Metrics: Daily Active Users, Daily User Growth, Daily Transaction Count, Daily Protocol Fee

Lending: TVL, Daily Borrowing Volume, Daily Deposits Volume, List of Depositors, List of Borrowers,

Do you agree to remove team-controlled wallets from all milestone metrics AND exclude team-controlled wallets from any incentives included in your plan: Yes

Did you utilize a grants consultant or other third party not named as a grantee to draft this proposal? If so, please disclose the details of that arrangement here, including conflicts of interest: No

SECTION 2b: PROTOCOL DETAILS

Is the protocol native to Arbitrum?: No

On what other networks is the protocol deployed?: Ethereum, Mantle, Telos, Evmos, Neon, Linea

What date did you deploy on Arbitrum mainnet?: 10/17/2023 - Arbitrum One Transaction Hash: 0x6c85d4329d... | Arbitrum One

Do you have a native token?: Not yet

Past Incentivization: What liquidity mining/incentive programs, if any, have you previously run? Please share results and dashboards, as applicable? n/a

Current Incentivization: How are you currently incentivizing your protocol?

MYSO has introduced its on-chain MYSO Activity Points program, offering rewards to borrowers, lenders, and those who refer others. The program includes various special boosters, such as extra points for borrowing from certain vaults or holding specific soulbound tokens, making it a highly adaptable scheme.

It’s essential to underscore that the program, launched two months ago and available solely on Mantle, is designed with a borrower-centric approach. Despite its recent inception, the program has already demonstrated promising results across all key metrics.

Acknowledging the need for a comprehensive strategy, our future incentives are set to target not just borrowers but every stakeholder involved. This aims to foster a more equitable and thorough program, designed to boost broader involvement and interaction.

Have you received a grant from the DAO, Foundation, or any Arbitrum ecosystem related program? No

Protocol Performance:

- October 2023: Launched MYSO v2 and enabled customized lending markets for leading platforms such as Mantle, Pendle, RocketPool, Gains Network, Lybra Finance, Threshold Network, and Mozaic.

- January 2024: Introduced fully customizable on-chain covered calls and conducted several transactions with treasuries (Telos, Evmos, Threshold Network) as well as with whales (Liquity, Beam, DIA, Holo), reaching a total trading volume of approx. $1m in notional.

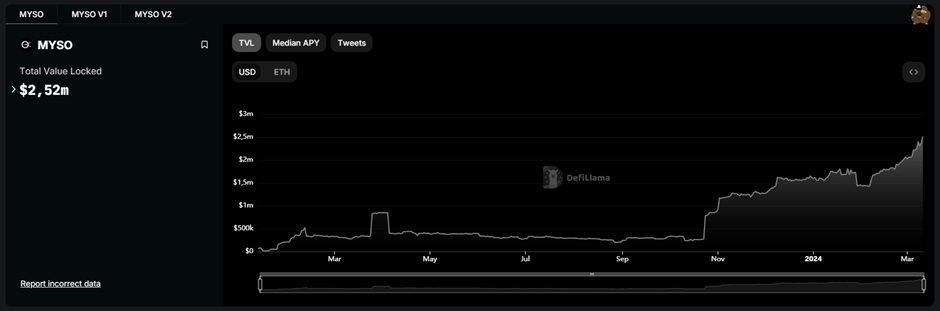

- Current TVL (as of 03/11/2024): $2.52m

Protocol Roadmap:

The main focus over the next 12 months revolves around significant enhancements and expansions within our protocol, as outlined below:

Bespoke Loans: Our primary aim is to empower an increasing number of protocols to establish their own customized lending markets. This initiative is designed to cater specifically to the unique needs of different communities and protocols, thereby broadening the accessibility and flexibility of MYSO.

Covered Calls: We are set to scale our covered calls to accommodate protocols, founders, and whales, making these financial instruments more accessible and efficient. In addition to this, we plan to introduce covered calls for retail users, democratizing access to more sophisticated financial strategies previously reserved for more experienced or institutional participants.

General Developments: An important upcoming milestone is the planned TGE in Q2 2024, which shall bolster growth and adoption of the protocol.

| Audit History & Security Vendors: | |

|---|---|

| – | Trail of Bits: publications/reviews/2023-04-mysoloans-securityreview.pdf at master · trailofbits/publications · GitHub |

| – | Statemind: public-audits/Myso Finance/2023-08-15_Myso_v2.pdf at main · statemindio/public-audits · GitHub |

| – | Omniscia: Omniscia Myso Finance Audit |

Security Incidents: None

SECTION 3: GRANT INFORMATION

Requested Grant Size: 100’000 $ARB

Justification for the size of the grant: Loans on MYSO can be structured with a conversion feature (similar to convertible bonds in TradFi). This allows DAOs/borrowers to serve repayments in their pledged collateral (typically a protocol’s native token) rather than in stablecoins, thereby reducing overall stablecoin borrowing costs. Furthermore, DAOs/borrowers can access the necessary liquid capital to extend their runway and achieve their roadmap goals, whilst limiting emissions, sell pressure and staying highly aligned with the community.

On the other hand, convertible debt also attracts willing lenders (e.g. from the DAOs community) who want to have equity-like upside participation in the collateral token.

In addition, arrangers can leverage their network and facilitate successful matches between borrowers and lenders, earning fees for each successful match. An arranger’s role is pivotal not only in connecting lenders and borrowers, but also in negotiating, completing, and finalizing deals to benefit all parties, overseeing the process from start to finish.

A crucial insight from our ongoing incentive program is the importance of incentivizing every stakeholder to maximize the outcome:

1) Incentivize DAOs/Protocols to borrow stablecoins through convertible debt

During this 12-week LTIPP program, the goal is to attract at least 2 new DAOs willing to borrow stablecoins through this novel primitive of convertible debt. Given our prior collaborations with DAOs (see also execution strategy) attracting two DAOs should be well within reach.

We anticipate that each DAO will seek to raise about $1.0m in debt, culminating in a total loan volume of $2m over the 12 weeks.

To encourage DAO participation, the grant shall cover their borrowing expenses, essentially allowing them to borrow at no cost. It is projected that each DAO will borrow funds for around 9 months at an interest rate of 12% p.a..

Calc Breakdown: $2m x 12% APY x (9/12 months) = $180k

2) Incentive Lender to deposit funds into MYSO

We will also focus on incentivizing lenders to deposit funds into a MYSO pool during the first 10 weeks of the LTIPP program, before the subscription period (i.e. a lender can subscribe to a specific DAO deal) commences. To achieve this, we expect that an average APY subsidy of around 15% is necessary.

Calc Breakdown: $2m x 15% APY x (10/52 weeks) = $60k

3) Incentive Arrangers to onboard DAOs

Recognizing the challenge of attracting DAOs, we will also incentivize third-party arrangers (e.g. Gauntlet) for successfully onboarding DAOs. We expect one successful DAO onboarding through an arranger and will pay a 2.5% commission, in line w/ market standards:

Calc Breakdown: $1m x 2.5% commission = $25k

The total rewards are therefore estimated to be $265k, where 75% shall be covered through $ARB rewards and the remaining 25% through $MYSO rewards.

ARB Rewards: 75% * $265k = $200k (or approx. 100k $ARB)

Please note, for all calcs we assumed ARB/USD @ 2.00.

Grant Matching: Yes, the remaining rewards of approx. $65k shall be paid in $MYSO.

Grant Breakdown:

As outlined above, the objective is to onboard at least two protocols during this 12-week LTIPP incentive program. We are convinced that this allows us to successfully position this new convertible debt narrative within the market. Below a detailed overview of the budget breakdown:

- 67.5k in $ARB and $45k in $MYSO: Leveraging MYSO’s strong connections with several DAOs in the Arbitrum ecosystem, these funds will be used to incentivize DAOs to borrow funds through a convertible bond by covering their interest expenses, making these transactions cost-neutral for the DAOs.

- 22.5k in $ARB and $15k in $MYSO: To encourage lenders to place their funds into a MYSO pool for up to a 10-week period before the start of subscriptions, we anticipate needing an average APY subsidy of about 15% p.a.

- 10k in $ARB and $5k in $MYSO: Recognizing the challenges in attracting DAOs, we plan to incentivize third-party arrangers with a 2.5% commission for each DAO they successfully bring on board.

Funding Address: 0xD6f15a797C78f598bcb840464151aC526dDD4A0f

Funding Address Characteristics: 3/7 multisig-setup

Treasury Address:

- Mainnet Treasury Address: 0x0d88B300134210FC94328C3269015c9831440F52

- Mantle Treasury Address: 0x8E2Dd4d57dF7E3480ABFe0eACa1c0Ccd41F1E18E

Contract Address: will be provided later

SECTION 4: GRANT OBJECTIVES, EXECUTION AND MILESTONES

Objective: The primary objective of the grant is to establish a leading marketplace for convertible debt on Arbitrum.

Execution Strategy: To achieve our goal of enabling at least two DAOs to raise approximately $1m each in convertible debt, our strategy allocates incentives as follows:

- Borrowers/DAOs shall receive the incentives to offset their borrowing costs. The incentives shall be paid out after the convertible debt deal has been closed, i.e. after the funds from the lenders have been transferred to the respective DAO. These incentives can be utilized by the DAO to either cover the interest payments, to further incentivize the current lenders or to incentivize future lenders for another convertible loan. Also worthwhile to highlight that we have a strong foundation of collaborations with multiple DAOs (including Evmos, Threshold, Pendle, Mozaic etc.) and promising leads for these convertible bonds, making the attraction of at least two additional DAOs a realistic target.

- Lenders will receive incentives as compensation for the opportunity cost of depositing their funds into a MYSO pool. However, these rewards can only be claimed at the conclusion of the subscription period and are contingent upon the lender participating in a deal with a borrower. If a lender opts not to participate in a deal, they will only be eligible to claim 10% of the potential rewards. This policy ensures lenders are genuinely committed to the process, preventing any gaming of the system through brief fund deposits followed by withdrawals.

- Arrangers will be receiving rewards for successfully onboarding DAOs to the platform. The payout shall happen once the deal is closed, i.e. the funds have been transferred to the respective DAO. In a manner akin to Gauntlet’s role as a “risk curator” on Morpho, they could also serve as an arranger on MYSO, orchestrating compelling transactions on the platform.

What mechanisms within the incentive design will you implement to incentivize “stickiness” whether it be users, liquidity or some other targeted metric? There are several ways on why the grant incentivizes “stickiness” over the long run:

- By introducing convertible debt to two DAOs, we expect to showcase the convertible debt instrument and its advantages within the broader ecosystem. This strategy is expected to naturally attract more DAOs to participate, even in the absence of incentives.

- Initially, incentives are provided to Arrangers as a subsidy to become acquainted with convertible debt. Subsequently, they stand to earn a significant income by successfully arranging deals between DAOs and lenders (e.g. an arranger always receives a percentage amount of the successfully facilitated loan). This creates a strong financial incentive for them to continue participating and contributing to the platform’s growth well beyond the initial incentive period.

- As DAOs will also be receiving a large portion of this grant, we will strongly encourage them to use the funds to incentivize lenders for e.g. a subsequent convertible bond, creating a self-reinforcing cycle of growth even post-LTIPP program (could also be enforced on-chain).

These approaches aim to create a self-sustaining ecosystem, where the value of convertible debt and the earning potential for arrangers drive long-term engagement and organic growth.

Specify the KPIs that will be used to measure success in achieving the grant objectives and designate a source of truth for governance to use to verify accuracy.

To effectively measure the success of the grant objectives, the following KPIs will be utilized:

- TVL / Lender Deposits Growth: The target is a minimum of $2m in deposited assets, with at least 90% of these assets being subscribed to a subsequent deal. This KPI is crucial because it directly reflects the liquidity and financial engagement within the platform, indicating the confidence and participation level of lenders. It demonstrates the platform’s ability to attract and retain capital.

- Number of Borrowers: Achieving at least two participating DAOs as borrowers. This KPI measures the platform’s success in attracting borrowers, specifically DAOs interested in the convertible debt model, and indicates market demand for this financial product. Reaching this target signifies that the platform offers a valuable and sought-after service, meeting its objective of fostering innovation in convertible debt financing.

- Number of Arranger Payouts: The goal is at least one arranger facilitating one of the two deals. This KPI highlights the platform’s effectiveness in engaging arrangers and leveraging their networks to connect borrowers and lenders. It signifies the active participation of third-party arrangers in the ecosystem and their contribution to achieve “stickiness”.

Source of truth for all above mentioned KPIs are on-chain data. More than happy to provide respective Dune dashboards during the LTIPP program.

Grant Timeline and Milestones:

To align with our grant execution strategy, the timeline and milestones are structured as follows:

-

Milestone 1: Initiation and Onboarding (Weeks 1-4)

- Objective: Secure initial lender deposits

- KPIs:

- TVL reaches at least $500k

- ARB Rewards: 6’000 $ARB

-

Milestone 2: Growth and Engagement (Weeks 5-8)

- Objective: Increase lender deposits and onboard a first DAO

- KPIs:

- TVL reaches $1.5m

- Onboard the first DAO interested in convertible debt

- ARB Rewards: 45’000 $ARB

-

Milestone 3: Expansion and Subscription (Weeks 9-12)

- Objective: Achieve full subscription of lender deposits, onboard a second DAO (via third-party arranger)

- KPIs:

- TVL reaches the target of $2 million, with at least 90% subscribed to deals

- Second DAO is successfully onboarded, facilitated via a third-party arranger

- ARB Rewards: 49’000 $ARB

-

Final Outcome: Program Assessment and Reporting (Week 12)

- Objective: Evaluate the overall success of the grant, based on the achievement of KPIs and the impact on the ecosystem

As outlined in the execution strategy, the rewards shall be paid out after the two convertible loan deals are executed, i.e. approx. after 10-12 weeks.

How will receiving a grant enable you to foster growth or innovation within the Arbitrum ecosystem?

Receiving this grant will empower us to stimulate growth and innovation within the Arbitrum ecosystem by enabling projects to raise (convertible) debt directly on Arbitrum. It will also allow these projects to leverage their token treasuries effectively as collateral and provide their users with potential upside through a bond conversion feature. This approach not only supports the financial structuring of projects within the Arbitrum ecosystem but also enhances the overall utility and engagement of Arbitrum users.

Do you accept the funding of your grant streamed linearly for the duration of your grant proposal, and that the multisig holds the power to halt your stream? Yes

SECTION 5: Data and Reporting

Is your team prepared to comply with OBL’s data requirements for the entire life of the program and three months following and then handoff to the Arbitrum DAO? Are there any special requests/considerations that should be considered? Yes, happy to comply with these data requirements

Does your team agree to provide bi-weekly program updates on the Arbitrum Forum thread that reference your OBL dashboard? Yes

Does your team agree to provide a final closeout report not later than two weeks from the ending date of your program? This report should include summaries of work completed, final cost structure, whether any funds were returned, and any lessons the grantee feels came out of this grant. Where applicable, be sure to include final estimates of acquisition costs of any users, developers, or assets onboarded to Arbitrum chains. (NOTE: No future grants from this program can be given until a closeout report is provided.) Yes

Does your team acknowledge that failure to comply with any of the above requests can result in the halting of the program’s funding stream?: Yes