Following our proposal to buy back $ARB tokens with the support of an institutional fund, the DAO community expressed interest in seeing evidence that the $ARB token is undervalued.

To respond to the community’s request, our team conducted an in-depth study on the undervaluation of $ARB tokens, the results of which you can see below in our article “9 Advantages of Arbitrum Over Other Blockchains.”

9 Advantages of Arbitrum Over Other Blockchains

1. Arbitrum’s TVL-to-Market Cap Ratio Outperforms Every Other L2

Source: Data from DefiLama & Coingecko

TVL to Market Cap ratios for Arbitrum and other Layer-2 networks (higher indicates more TVL per unit of market cap). Arbitrum (blue) significantly outperforms the others.

Arbitrum holds much more money (TVL) on its network than other similar ones, but its token isn’t as expensive.

Think of it this way:

- Arbitrum has $2.44 billion locked up. That’s more than double what Polygon has ($1.04 billion) and six times more than Optimism ($367 million).

- Even with all that value, Arbitrum’s market price (its “market cap”) is only about $1.5 billion.

This means that for every dollar of Arbitrum’s market price, the network is actually holding $1.62 in value.

Compare this to its competitors:

- For every dollar of Polygon’s market price, it only holds about $0.65 in value.

- For Optimism, it’s only about $0.39 in value for every dollar of its market price.

2. Arbitrum TVL-to-Market Cap Ratio Outperforms Every Other Blockchain Tokens

Arbitrum’s token ($ARB) is doing a lot more work for its price than other similar tokens. Even if you look at the total possible value of all tokens (fully diluted), Arbitrum still comes out on top.

This suggests that $ARB might be undervalued. Investors are currently paying less for the value stored on Arbitrum compared to other networks.

Source: Data from DefiLama & Coingecko

Moreover, when we expand our view to include all top blockchains by market cap, Arbitrum still stands out! None of the leading chains comes close to its 1.62 TVL-to-market-cap ratio, underscoring just how underappreciated $ARB remains even on a CMC-wide scale.

3. Arbitrum’s Stage 2: Outpacing Competitors in Decentralization

According to data from L2BEAT, Arbitrum’s closest competitor by TVL is Base. According to our analysis, when Base issues its token, its FDV could reach $30 B or even higher, significantly above Arbitrum’s current FDV of just $3 B.

Total value secured is calculated as the sum of canonically bridged tokens, externally bridged tokens, and native tokens.

Source: Data from L2BEAT

Arbitrum is nearing Stage 2 decentralization, a first for any L2, making it the most secure and mature L2 solution by industry standards. This transition significantly reduces risk for large institutions, assuring them of the network’s security, stability, and censorship resistance.

When Arbitrum achieves Stage 2 status and also performs a big token buyback supported by major institutions, it will gain a huge competitive edge over other L2s, including BASE. This will clearly establish Arbitrum as the top choice for both its technology and its financial approach.

4. Is Arbitrum The Most Undervalued Blockchain on The Market?

Arbitrum shows strong fundamental metrics regarding network activity.

- User Activity: Arbitrum is ranked 6th in weekly active users, with 1.4 million users engaging with the network.

- Transaction Volume: It secures the 4th position in daily transaction count among competing blockchains, processing 2.4 million transactions in a 24-hour period.

Source: Data from Token Terminal

Market Position:

Arbitrum is very active, but its market value is surprisingly low at just $1.7 billion. It’s much cheaper than other big names, and even valued similarly to some competitors, it actually uses more. This means the market might not fully see how good Arbitrum really is yet.

5. DEX Volume

DEX Trading Volume (24h): Arbitrum demonstrates strong leadership in DEX trading volume, reaching around $931.9M per day, significantly outperforming major ecosystems like Sui ($704.8M), Avalanche ($675.4M), Aptos ($188.9M), Polygon ($187.8M), and Tron ($182.8M). This highlights the high level of activity and liquidity within Arbitrum’s DeFi ecosystem. High DEX volume is a strong indicator of genuine DeFi usage, as users are actively trading and investing on Arbitrum. (By contrast, raw transaction counts can be misleading – some chains inflate tx counts via airdrop farms or games – so DEX volume is a more reliable gauge of real activity.)

Source: Data from DefiLama

Importantly, the numbers show Arbitrum is used for real things, not just quick trades. Its high trading volume and large locked value mean people are really using it for lasting transactions and economic activity. As experts say, how much people trade on a blockchain shows how important it is for DeFi. Even though Arbitrum is one of the top five blockchains for daily trading, its market value is much lower – it’s only ranked 58th, not even in the top 50.

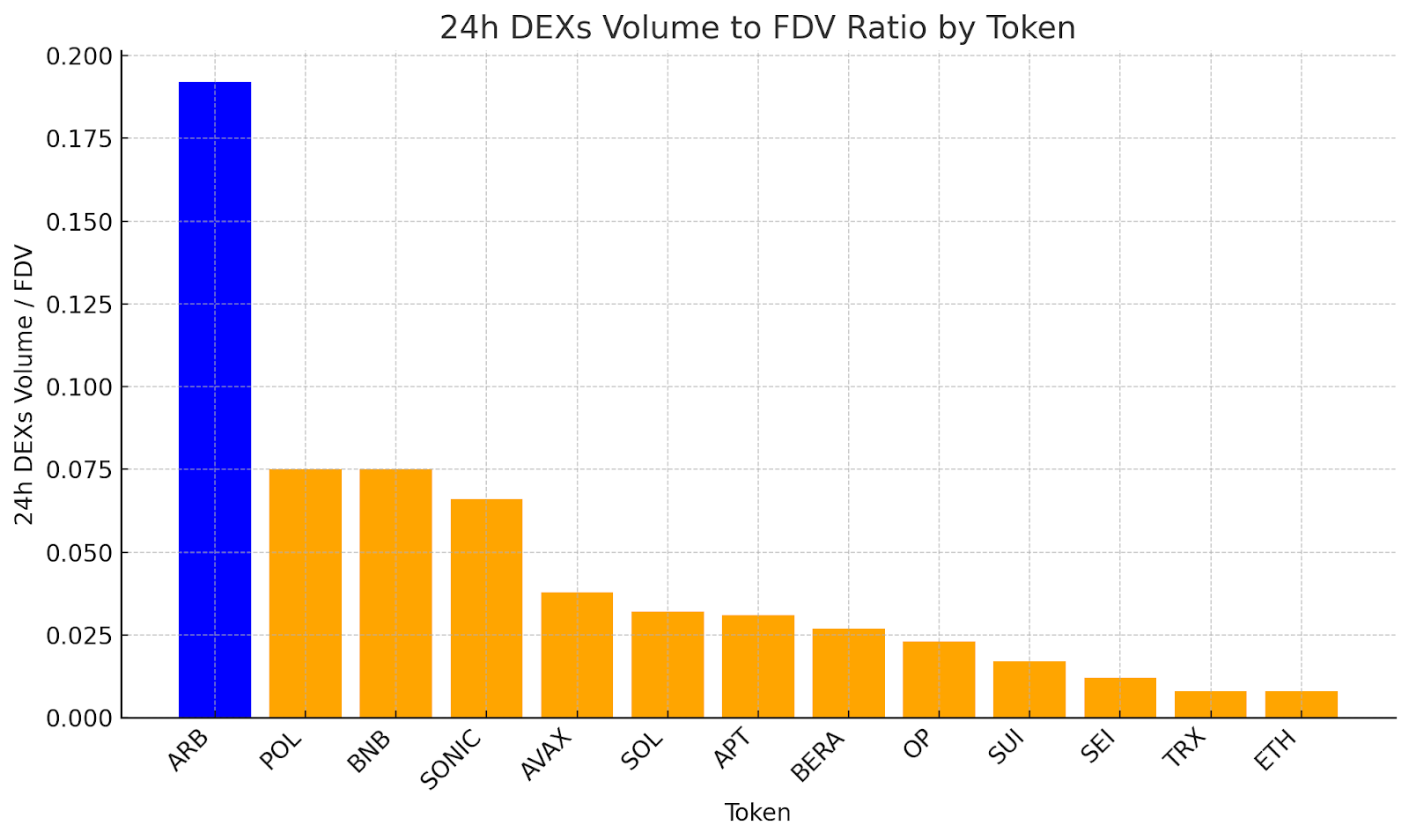

6. DEXs Volume to FDV Ratio: Arbitrum Leads by a Huge Margin

The chart of the 24-hour DEXs Volume to Fully Diluted Valuation (FDV) ratio is a key indicator of capital efficiency and a token’s real-world utility. It shows how much trading activity a token generates relative to its total potential value.

Source: Data from DefiLama & Coingecko

As seen on the chart, Arbitrum (ARB) shows an outstanding result, significantly outpacing all other tokens.

- Arbitrum’s Leadership: With a ratio of almost 0.19, Arbitrum demonstrates unprecedented trading activity relative to its fully diluted valuation. This figure is more than double the ratio of its nearest competitors on the chart, such as POL and BNB, which have a ratio of about 0.075.

- Comparison with Competitors: Other major blockchains like Solana (SOL), Avalanche (AVAX), and Ethereum (ETH) have significantly lower ratios. This suggests that while their total valuations may be high, their tokens do not generate the same level of trading activity on DEXs for every dollar of their value.

This high ratio for ARB is further compelling evidence that the Arbitrum ecosystem not only attracts significant liquidity but is also actively used for real economic activity. While other projects may have high valuations on paper, Arbitrum proves its value through real-world use and a high velocity of its token, which supports the thesis of its potential undervaluation by the market.

7. Arbitrum’s Strong Developer Community

Arbitrum stands out as the most developer-efficient blockchain according to the DEV/MCAP ratio a metric that compares the number of active developers to the project’s market capitalization. With a ratio of 0.00000035117, Arbitrum ranks significantly higher than even major ecosystems like SUI, Solana (SOL), Ethereum (ETH), Hyperliquid (HYPE), and TRON (TRX).

Source: Data from Electric Capital Developer Report

This exceptional efficiency reflects not just the productivity of the Arbitrum ecosystem, but also how undervalued it may be relative to its builder activity.

Arbitrum’s large and active developer community shows that it’s a strong and trusted platform. Developers choose Arbitrum because it has real users, good growth, and lots of opportunities to build. The fact that thousands of developers contribute to Arbitrum shows confidence in the ecosystem. More developers mean more apps and tools, which brings in even more builders and users. Arbitrum has become a developer-friendly blockchain, and that helps it grow faster and stay strong in the long term.

Source: Data from Developer Report by Electric Capital

Full-time developer counts across leading blockchain ecosystems further highlight Arbitrum’s edge. Arbitrum boasts roughly 274 core (full-time) developers – the highest among the chains compared. This surpasses the full-time developer bases of other major platforms such as NEAR (~240), Optimism (~187), and Avalanche (~173), and dwarfs newer ecosystems (some have only ~10 core devs). Arbitrum’s ability to sustain the largest full-time developer team underscores its strong builder appeal and the depth of commitment within its ecosystem.

8. Analysis of Protocol Count: Arbitrum’s Ecosystem Strength

Data from DeFiLlama provides valuable insights into the distribution of decentralized finance (DeFi) protocols across various blockchain networks, covering both the broader blockchain landscape and the specific segment of Layer 2 (L2) solutions.

As of the latest available data, Arbitrum ranks as the #1 Layer 2 blockchain and #3 overall among all blockchains by the number of hosted DeFi protocols, with 830 active projects. This places Arbitrum among the top blockchain ecosystems, trailing in protocol count only behind industry giants Ethereum and BNB Smart Chain (BSC).

This high concentration of protocols reflects strong developer interest and confidence in Arbitrum’s infrastructure. The large number of active projects is a clear indicator of a vibrant and healthy ecosystem, reinforcing Arbitrum’s position as a leading platform for building decentralized applications.

Source: Data from DefiLama

To assess an ecosystem’s efficiency at attracting developers relative to its market valuation, one can analyze the protocol count to FDV ratio. This metric shows how “cheaply” the market gets to support a large number of projects on the network.

Source: Data from DefiLama & Coingecko

And here, Arbitrum once again shows exceptional results. With a ratio of almost 1.85, ARB is significantly ahead of all competitors, including SONIC (≈1.3) and OP (≈1.0). This proves that Arbitrum not only has one of the largest numbers of protocols in absolute terms, but is also the most efficient platform at supporting them relative to its valuation, which again highlights its strong fundamental position.

9. A Strategic Plan for Arbitrum: How to Attract Up to $5B and Multiply the Value of $ARB Using a Proven Wall Street Model

Introduction: A New Way to Attract Capital

In today’s crypto market, old methods for raising capital aren’t as effective as they used to be. This is where smart, new financial strategies come in. Top investment funds like Consensys, Electric Capital, Parafi, and Galaxy Digital have shown a brilliant way to overcome market fatigue and create incredible value. They developed and executed a plan that allowed them to achieve an effective valuation of $16,700 per ETH.

This isn’t just a theory; it’s a real-world case study that the Arbitrum DAO can adapt to attract $500 million to $5 billion in capital and drive massive growth for the $ARB ecosystem.

The Core Strategy: A Genius Bridge Between DeFi and TradFi

Instead of just relying on retail investors in a volatile market, these funds built a multi-step strategy to turn their ETH holdings into a high-growth stock market asset. You can think of it as creating a “MicroStrategy for Ethereum,” and it serves as a perfect model for Arbitrum.

Here’s a simple breakdown of how this smart strategy worked:

- Form a Strategic Alliance. A group of top funds pooled $425 million to buy a large stake in a publicly traded company on the Nasdaq stock exchange (SharplinkGaming) at $6.15 per share.

- Convert Digital Assets to Cash. To fund the purchase, the funds strategically sold ETH through private, over-the-counter (OTC) deals for $425 million. At the time, ETH’s market price was $2,646. This was a smart move to get cash without causing the market price to drop.

- Create a New Story. Immediately after the purchase, they launched a major communications campaign. They presented the public company to investors as the new “Ethereum Treasury Vehicle” on Nasdaq. This captured the attention of traditional investors who are more comfortable buying stocks than tokens.

- Start the Growth Flywheel. This new and exciting story created a buzz around the company’s stock. As interest and the stock price grew, the company issued new shares to raise more money. This new capital was then used to buy ETH from the market for its treasury, creating more demand for ETH and strengthening its own balance sheet.

- The Amazing Result. In just six weeks, the company’s stock price shot up 6.3 times, hitting $39.08 per share. As a result, the ETH that was originally valued at ~$2,600 was now indirectly worth $16,700 per coin on the public company’s balance sheet. The funds didn’t just make a huge profit, they set a new precedent.

The Opportunity for Arbitrum: Repeat and Outperform

This strategy is not about market manipulation; it’s about smart financial planning. It’s a way to “package” the value of a digital asset into a format that traditional capital understands and wants: a stock in a public company.

How can the Arbitrum DAO do this?

- Create an "Arbitrum Treasury Vehicle." The DAO community could start or acquire a public company (like a SPAC) to become the official treasury fund for Arbitrum on a major stock exchange.

- Strategic Funding. A portion of the DAO’s treasury, or funds raised from strategic partners, could be used to make the initial purchase of $ARB to fill the company’s balance sheet.

- Attract Institutional Capital. By positioning this company as the main bridge for traditional investors to enter the Arbitrum ecosystem, it would attract a huge flow of capital from pension funds, family offices, and everyday stock investors looking to get exposure to $ARB’s growth.

- The Value Growth Cycle. A rising stock price would allow the company to raise more capital, which would then be used to systematically buy more $ARB from the market. This creates constant, strong buying pressure and increases value for all token holders.

Final Thoughts: A Vision for the Future

The funds that did this with ETH proved that an asset’s price on an exchange is only part of the story. With strategic thinking, you can build much greater value on top of it. They achieved a 6.3x multiplier on the effective value of their assets.

If the Arbitrum DAO adopts this idea, $ARB could see similar or even greater growth. This isn’t just a way to increase the price; it’s a fundamental step toward integrating Arbitrum into the global financial system, making $ARB a key asset in both the DeFi world and the portfolios of traditional investors. This is a bold idea, worthy of a forward-thinking community like Arbitrum.

Conclusion

The data presented unequivocally demonstrates that Arbitrum is a market leader whose fundamentals significantly outpace its current market valuation. Across all key metrics, Arbitrum shows clear superiority not only over other L2 solutions but also over many of the top blockchains. This gap between the ecosystem’s true strength and its market price represents a clear anomaly.

Whether it’s capital efficiency (TVL‑to‑Market‑Cap ratio), genuine economic activity (leading DEX Volume‑to‑FDV ratio), or the most robust developer and protocol ecosystem among L2s, Arbitrum consistently proves its superiority. While competitors are often valued higher on the strength of marketing, Arbitrum backs its value with real usage and sustained on‑chain activity.

This undervaluation is not a weakness but our greatest opportunity, making $ARB one of the most attractive assets with enormous growth potential. The proposed strategic plan, based on a proven Wall Street model, is the logical next step to close this valuation gap. Executing this plan will not only attract significant capital but also cement Arbitrum’s status as the undisputed industry leader it deserves to be.

For easier review of the analytics, you can view the report in PDF format “Quantitative Proof of Arbitrum Undervalued Token”