Name

Etherfuse

Address (Headquarters)

Address: Blvd. Adolfo López Mateos 172, Int. 2

Col. Merced Gómez

Benito Juárez, Ciudad de México, México

C.P. 03930

Website

Primary contact Name

Title

CEO

Country

Mexico

Email, Telegram, Forum, & other methods of contact

Email: contact@etherfuse.com

Telegram: etherfuse

Key Information

Expected Yield

4- 12%

Expected Maturity

Bonds mature weekly to monthly depending on the underlying asset

Underlying asset

Short Term US Treasuries

Short Term Mexican Treasuries

Short-term British Gilts

Short-term Brazilian treasuries

Minimum/Maximum transaction size

$1 - 100MM

Current AUM for product

5MM

Current AUM for issuer

5MM

Volume of transactions LTM

10MM

Source of first-loss capital

These bonds are risk free short-term treasuries issued by sovereign governments

Basics and background

1. How will this investment improve Arbitrum’s RWA ecosystem?

Etherfuse brings the further decentralization of restriction free, risk free products, regulated and operated out of Mexico. Etherfuse enables Arbitrum to decentralize their treasury from asset issues and is regulated in the West by bringing the optionality of treasuries from emerging markets in addition to those in the EU, British Isles and US territories.

We currently are the only compounding treasury asset issuer with LATAM assets regulated out of LATAM.

2. Identify key management personnel and individual experience. Also include third parties utilized for managing assets and their qualifications.

The custodians of Etherfuse®’s Financial Assets include BBVA México, Actinver Casa de Bolsa, and Kuspit Casa de Bolsa. All institutions are financially stable and authorized by Mexican regulators.

As a context:

- BBVA México, S.A., Institución de Banca Múltiple, Grupo Financiero BBVA México- As of November 1, 2024, this financial institution has a capitalization index of 19.57%, being in category I, i.e., without solvency problems and therefore not subject to any type of special preventive and/or corrective measures before the financial authorities. (Source)

Its authorization can be found here - Actinver Casa de Bolsa, S.A. de C.V., Grupo Financiero Actinver- As of November 1, 2024, this financial institution has a capitalization index of 15.23%, being in category I, i.e., without solvency problems and therefore not subject to any type of special preventive and/or corrective measures before the financial authorities. (Source)

Its authorization can be found here and here - Kuspit Casa de Bolsa, S.A. de C.V.- As of November 1, 2024, this financial institution has a capitalization index of 96.23%, being in category I, i.e., without solvency problems and therefore not subject to any type of special preventive and/or corrective measures before the financial authorities. (Source)

Its authorization can be found here

6. Describe any previous work by the entity or its officers/key contributors similar to that requested. References are encouraged.

We’ve issued treasury-based assets since Nov 2022.

Co-founders Dave and AJ have deep experience in cryptography, payments and security with Apple, Boeing and Neural Payments

Dave Taylor: David Taylor - etherfuse | LinkedIn

References:

AJ Taylor: https://www.linkedin.com/in/aj-taylor-977a5481/

7. Has your entity or its officers/key contributors been subject to an enforcement action, criminal action, or defaulted on legal or financial obligations? Please describe the circumstances if so.

NO

8. Describe any conflicts of interest for your entity and key personnel.

None

9. Insurance coverages, guarantees, and backstops Name of insurer or guarantor Per incident coverage Aggregate coverage

With financial institutions, Etherfuse® enters brokerage agreements to manage and secure assets. For customers, the Agreement for the Provision of Services and Commercialization of Tokens outlines their ownership rights, including access to the Stablebonds and their associated claims.

As a context, with the financial institutions that are custodians of the Financial Assets, Etherfuse® enters into a brokerage agreement through which Etherfuse® grants a mandate for the performance of brokerage acts in the securities market, consisting of the execution of purchase, sale, custody, administration and deposit orders of such assets.

An Agreement for the Provision of Services and Commercialization of Tokens is entered into with the customers under which Etherfuse® provides an internet platform which it administers and allows its customers to acquire Stablebonds upon payment by the customer through USDC. The Agreement provides the customer with the right to claim: (i) the nominal value of the Financial Asset backing the Stablebond; as well as (ii) the Rewards linked to the holding of the Stablebond. The token holders are considered as owners of the Stablebonds and as such may exercise the rights of use and disposition of the Stablebonds, terms and conditions apply.

10. Historical tracking error in your proposed product, or similar to that being proposed Product 2024 YTD 2023 2022 2021

None

11. Brief reason for above tracking error

N/A

12. Please describe any experience your firm has in working with decentralized organizational structures

Past DAOs with Jupiter, Etherna, Maker

13. What is your entity’s current assets under management, assets held in trust, total value locked, or equivalent metric for your legal structuring?

Financial Assets backing Stablebonds are held with authorized Mexican financial institutions. Etherfuse® has an internal policy that requires it to distinguish between its own investments and customer funds, this is dully reflected in its financial statements. Regular attestation reports ensure transparency and accurate reserves.

As a context, on a regular basis, an independent third party to Etherfuse® issues attestation reports focused in a process that aims on verifying the accuracy and control of Etherfuse®’s reported reserves of Financial Assets that back the Stablebonds based on cryptographic proofs provided by Etherfuse® in public blockchains, the reconciliation of these proofs with Etherfuse®’s internal records, interfaces and account statements issued by financial entities in Mexico.

14. How many of these assets held are present on Arbitrum One, if any?

Launching Arbitrum One January 2025

Plan design

Please describe your proposed product, including a description of the underlying assets and, if more than one asset, the proposed allocation among assets and general investment guidelines. Where appropriate, include targeted maturity mix and credit quality. Attach supplementary documents as appropriate.

40% US AA+, 20% Cetes BBB+, 20% Tesouros BB, 10% Gilts AA, 10% EU Bonds AAA

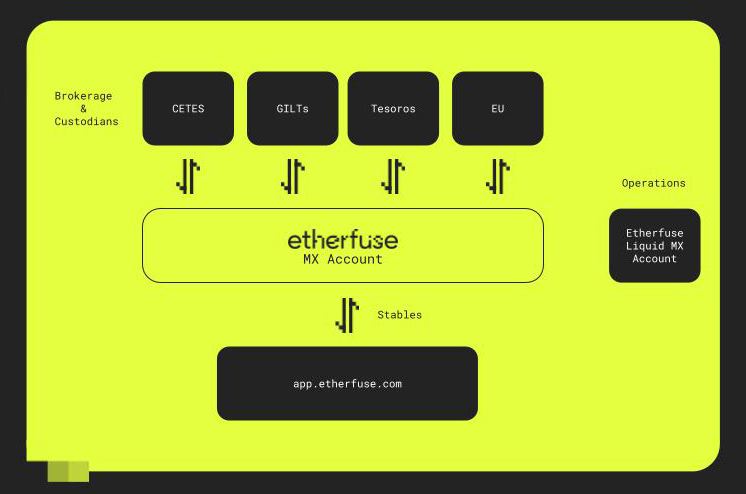

Stablebonds are digital assets issued by Etherfuse®, backed by government debt instruments such as Mexican CETES, US Treasury Notes, or UK Gilts. The backing allows holders to claim both the nominal value of the underlying assets and the generated rewards.

As a context, Stablebonds are digital assets issued through blockchain technology, which are backed by different financial assets through financial entities authorized in Mexico to operate. These financial assets backing the Stablebonds currently are: (i) Mexican government debt (CETES); (ii) US government debt (US Treasury Notes); and, (iii) UK Government liability (Gilt) (hereinafter referred to indistinctly as “Financial Assets”).

The acquisition of each Stablebond generates the right in favor of its holder to claim: (i) the nominal value of the Financial Asset backing the Stablebond; as well as (ii) its accessories upon maturity of the Financial Asset, in its case.

The accessories are the amounts established by Etherfuse® through the Platform (hereinafter, “Rewards”), which source is the yield obtained on the acquisition of the underlying Financial Asset.

Do investors have any shareholder, investor, creditor or similar rights?

Describe the legal and contractual structuring for your product including regulatory bodies overseeing your business and the product and identifying all legal jurisdictions interacting with your product. Attach supplementary documents as appropriate.

Etherfuse Liquid Mx, S.A.P.I. de C.V. (“Etherfuse Liquid”) is the only Mexican blockchain company with a resolution from the financial authority (CNBV) confirming that its Tokens do not require authorization, registration, or concession by financial regulators. This gives Etherfuse® a unique competitive advantage in the Mexican market.

As a context, Etherfuse Liquid initiated -before the National Banking and Securities Commission (“CNBV”) in Mexico- a procedure in order to be authorized (“Authorization Request”), in essence, to receive funds from the general public derived from the issuance and placement/trading of blockchain digital assets (“Tokens”) whose possession brings with it the right to claim payments to be made by Etherfuse®, arguing that the characteristics of the Tokens could update the definition of Security provided in the Securities Market Law (“SML”) whose public offering and placement requires prior authorization by the CNBV.

On April 16, 2024, the CNBV issued the Resolution P090/2024 through which, among other aspects, it states:

"1.- With respect to the Tokens… it was not identified … that such assets meet the formal or doctrinal elements of a credit title, nor the formal elements of a Security; nor the formal elements of an electronic title… therefore, it can be validly concluded that…:

Tokens do not constitute credit titles, since they do not comply with the formal requirements established in the General Law of Credit Titles and Credit Transactions.

The Tokens do not constitute Securities in terms of what is established by the SML, since, although they may share some of the characteristics of Securities, they do not comply with all the formal requirements of the SML, among which the most important are that they are not a credit title and that they are not susceptible to circulate in the markets regulated by said Law.

The Tokens do not constitute Electronic Titles in terms of article 282 of the SML, since they do not comply with the formal requirements established in Circular 36/2020 issued by Banco de México, among others, they are not susceptible to be deposited in a Securities Depository Institution.

“2.- … it continued to be noted that the services it intends - Etherfuse Liquid - to offer are not subject to any authorization, registration or concession in accordance with the Law to Regulate Financial Technology Institutions (“FinTech Law”) or any other financial law…”

Pursuant to the above, it can be concluded that: (i) the above consideration issued by CNBV is a definitive administrative act that puts an end to the procedure, therefore, the services that Etherfuse Liquid intended by the Authorization Requested does not require authorization, registration or concession by the Mexican financial regulator; (ii) the administrative act only applies to Etherfuse Liquid, giving it a competitive advantage in the Mexican market; and, (iii) in any case, Etherfuse Liquid must comply with the applicable general regulations, particularly those related to the prevention of money laundering and the treatment of personal data.

Based on the foregoing, Etherfuse Mx, S.A. de C.V. (“Etherfuse Mx” or “Etherfuse®”), as part of the same business group of Etherfuse Liquid, by reverse solicitation -that is, by means of a private and direct invitation- offers to its customers the entering into an Agreement for the Provision of Services and Commercialization of Tokens derived from which Etherfuse® makes available to them an internet platform that Etherfuse® manages allowing them -to its customers- the acquisition of Tokens issued by Etherfuse® (hereinafter, “Stablebonds”) upon payment made by the customer through USDC.

2. Would Arbitrum’s assets be bankruptcy remote from your own entity and its officers/key contributors? If so, please explain the legal and contractual basis. On a confidential, non-reliance basis, provide any third party legal opinions to support the conclusions.

If Etherfuse® were declared insolvent, customers have the right to separate their assets from the Etherfuse’s assets. Customers can also act as common creditors if asset separation is not possible.

As a context, in Mexico, the purpose of the Mexican Bankruptcy Law is to establish the procedural rules for: (i) the declaration of insolvency proceedings of merchants; (ii) the recognition, ranking and priority of credits owed by the merchant; (iii) the execution of payment agreements with the company’s creditors; and, in the event that the latter is not possible -among other cases- (iv) the declaration of bankruptcy of the merchants.

This legal framework is designed to ensure the preservation of the companies, to prevent the generalized noncompliance with payment obligations from jeopardizing the viability of the companies, with a portion of the merchant’s assets being subject to the payment of the unfulfilled obligations.

A merchant is declared in insolvency if it defaults in the payment of its obligations on a generalized basis and is requested by the merchant itself or, as the case may be, is sued by any creditor or the authority in charge of the investigation and prosecution of crimes (Public Prosecutor’s Office). The generalized default of payment consists of the non-compliance of payment obligations to two or more different creditors of the respective merchant and the following conditions are present:

- That there are overdue obligations with at least thirty days of expiration and that these represent thirty-five percent or more of all the obligations owed by the referred merchant as of the date on which the petition or request for the declaration of insolvency has been filed;

- The Merchant does not have assets to meet at least eighty percent of its past due obligations as of the date of filing of the claim or petition.

The assets that are considered for the purposes of the provisions of item b above are:

- Cash on hand and deposits;

- Time deposits and investments whose maturity does not exceed ninety calendar days after the date of filing of the claim or request;

- Clients and accounts receivable whose term to maturity does not exceed ninety calendar days after the date of filing the claim or request, and

- Securities for which purchase and sale transactions are regularly registered in the relevant markets, which could be sold within a maximum period of thirty banking days, whose valuation as of the date of the filing of the claim or request is known.

After the merchant has answered the claim, a visitor appointed by the Federal Judiciary Council goes to the merchant’s establishment and the court declares that the merchant is in general default of payment, then the declaration of the insolvency proceeding is issued.

After the referred declaration, the conciliation phase begins, as well as the recognition, graduation and priority of credits owed by the merchant.

In the event that such declaration is issued, the Mexican Bankruptcy Law provides an action of separation of assets that may be exercised by the merchant’s creditors in order for certain assets not to be considered as part of the assets with which the company will be liable before the other creditors.

In order for the above to be applicable, the referred law establishes that such assets in possession of the merchant over which the separation action is exercised must be: (i) identifiable; (ii) that the property of the corresponding assets has not been transferred to the merchant by a definitive and irrevocable legal title; and (iii) that the action is promoted by the legitimate owner of such assets.

Among the assets that may be subject to this separation action are those that have been received in administration, even if they have been exchanged for others by any legal title.

When the referred action is not applicable, the credits must be paid in the following order in terms of Articles 217, 221 and 224 of the aforementioned Law with the merchant’s assets:

- The credits in favor of the workers for salary or wages accrued in the last year and their indemnifications;

- Those contracted for the administration of the merchant’s assets or indispensable to maintain: (i) the ordinary operation; (ii) liquidity; (iii) security and/or asset expenses;

- Privileged creditors (derived from cases of death);

- Creditors with collateral (mortgage or pledge, duly registered in the corresponding public registry);

- Tax credits;

- Creditors with special privilege (who, according to the characteristics of the relationship, maintain a special right of retention, such as in the case of a lodging, consignment and/or transportation contract);

- Common creditors (all those who do not meet any of the aforementioned assumptions);

- Subordinated creditors (persons who have agreed to subordinate their rights with respect to the common credits, controlling companies or companies with a relationship in the administration of the company);

Based on the foregoing, if Etherfuse® becomes in general default of its obligations and is declared insolvent, its customers may:

- Exercise the action of separation of assets so that such assets will not be considered as part of the assets with which the company will respond to its creditors, arguing that the USDCs were transferred to Etherfuse in administration, so they are entitled to the Financial Assets to which they were exchanged.

- Appear as a Common Creditor, in the event that for any reason it is decided by the court that the aforementioned separation action is not admissible and its credit: (i) has been recognized by the conciliator based on the accounting and other information and documentation of Etherfuse® (“Provisional List”); or (ii) because it -the customer- requests it after the publication of the Provisional List.

How are Arbitrum’s assets protected vis-a-vis the bankruptcy of the brokerage or applicable financial institution (e.g., bank deposit insurance, securities insurance, etc.)?

Does the Issuer issue more than one asset? If so, what is the priority relationship between different asset classes?

Provide a detailed cash flow diagram that shows the flow of funds from ARB/Fiat conversion, investment in underlying asset, payment of expenses, sale of underlying asset, and repayment (Fiat/ARB conversion), including the counterparties and legal jurisdictions involved.

1. Describe anticipated tax consequences (if any) in transacting on the underlying and/or receipt of yield.

Etherfuse does not withhold taxes on behalf of the holder but defers the tax liability to the holder and their tax jurisdiction.

2. Describe the process and expected timeline for liquidation of assets, if given instructions to do so by Arbitrum governance.

In most cases immediately and in a worst case scenario 7 days

3. What amount of first-loss equity will Sponsor provide to ensure over-collateralization, how is the first-loss equity denominated, and what is the source of capital?

We currently provide 1.5MM in liquidity sourced from venture capital.

4. Describe the liquidity and stability of the proposed underlying assets, including anticipated settlement times from the sale of the underlying to the repayment of ARB.

Short-term treasuries are some of, if not the safest investment class in the world. The Mexican market alone has 600B in liquidity in the bond market. Settlement time is generally a few minutes during market hours.

5. If relying on the blockchain for any of the transactional flows, please describe any blockchain derived risks and mitigations.

Our assets are restriction free, however, we do require to KYC anyone who mint/burns directly from us at app.etherfuse.com. No other flow is required.

6. Does the product rely on any derivative product (swaps,OTC agreements?

No.

7. List all the third party counterparties linked to your assets including and not restricted to prime broker if any, custodian, reporting agent, banks for derivatives or loans and provide primary contact details for the third party counterparties

BBVA, Actinver, and Kuspit

8. Can you explain how is risk management (inv and operational) being done? Can you provide a copy of your risk management policy?

https://app.etherfuse.com/legal/asset-security

Performance reporting

1. What are your proposed performance benchmarks? If this is substantially different from the underlying assets, please explain why.

There is no difference between performance of our tokens and the underlying assets.

2. Describe the content, format, preparation process, and cadence of performance reports. This should include proof of reserves, if appropriate. Please include a sample report.

Proof of reserves, tax audits, financial audits, and AML audits

3. Who provides the performance reports in respect of the underlying assets?

We provide a third-part audit of all our reserves monthly

https://app.etherfuse.com/legal/proof-of-reserves

4. Describe any formal audit process and timing of such audits.

We do yearly financial and AML audits and monthly tax reporting provided by BHR

Pricing

1. Provide a copy of your standard contract, or one similar to what is being proposed here.

Standard Contract:

2. Fee summary: Inclusive of the full scope of services requested. Product Fee schedule If asset based Fee calculation for our plan if asset based Annual fee if flat fee Any other fees (including redemption or minting fees)

Etherfuse® generates revenue from:

- Commissions as a percentage of the Yields on Financial Assets acquired using customer funds, minus commissions charged by third parties and taxes.

- Yields on Financial Assets purchased with its own capital.

As a context, Etherfuse®´s commissions collection model is based on a variable structure. This structure is related to the yield (Y) of the underlying assets. The fee charged (f) ranges from 0.25% to 1.5%, based on the yield and risk level of the underlying asset as follows:

- Low yield range (Y < 4.5%): A fixed commission of 0.25% is applied to products with a yield equal to or less than 4.5%.

- Intermediate yield range: For products whose yield is in an intermediate range, the commission is calculated as follows:

F%=0.2273*Y-0.7727

This formula adjusts the commission proportionally to the performance of the asset, allowing the commission rate to increase as the performance increases.

- High yield range (Y > 10%): Products with yields equal to or greater than 10% are subject to a fixed fee of 1.5%.

The general model looks as follows:

Y < 4.5% = 0.25% | F%=0.2273Y - 0.7727 | Y10%=1.5%

3. Describe frequency of fee payment and its position vis-a-vis payment priority compared with other expenses (i.e., cash waterfall)

Fees are withheld each maturity, so no direct payment is necessary. All advertised yields go to the holder.

Smart Contract/Architecture

1. How many audits have you had and name of auditors? Please provide a copy of reports.

OttrSec

2. Is the project permissioned? If so how are you managing user identities? Any blacklisting/whitelisting features?

No, it’s not permissioned.

- Is the product present on several chains? Are there any cross chain interactions?

Solana, Stellar and now Arbitrum

4. Are the RWA tokens being used in any other protocols? Please describe the various components of the ecosystem

Lending, currency arbitration, and perps

5. How are trusted roles/admins managed in the system? Which aspects of the solution require trust from users?

The only trust needed is that of the legal entities and brokerages

6. Is there any custom logic required for your RWA token? If so please give any details.

NO.

Supplementary

1. Please attach any further information or documents you feel would help the screening committee or ARB tokenholders make an informed decision.