STIP Analysis of Operations and Incentive Mechanisms

The below research report is also available in document format here .

Introduction

The following analysis presents an overview of the final STIP fund allocation across different incentive mechanisms, focusing on any differences in growth trends and their sustainability for perp DEX and spot DEX protocols, while comparing activity on Arbitrum against other relevant ecosystems. Moreover, this analysis covers broader themes and recurring developments that have emerged through STIP applications, updates, recipients’ performance, and discussions with recipient teams.

TL;DR

- Following changes made to incentive allocations throughout the STIP, the most popular high-level mechanisms utilized were standard liquidity incentives (~30% of total allocation), fee rebates (~25% of total allocation), trading/points/usage-based programs (~12% of total allocation), liquidity incentives for native token(s) in pools on partner protocols (~8% of total allocation), and liquidity incentives with optional/required long-term/perpetual capital locking (~8% of total allocation).

- Most spot and perp DEX STIP recipients’ top-line metrics fell notably after the STIP ended and are currently around levels seen in September 2023. There are a few outperformers, generally younger, differentiated protocols that outgrew the market during the STIP and have successfully managed to maintain activity and capital in the long term.

- Excluding the outperformers, the absolute change in TVL/Volume achieved per ARB utilized to increase these metrics directly has widely converged between protocols in the same verticals.

- Overall, during the STIP, Arbitrum’s market share growth across major blockchains peaked at ~0% for TVL, ~5% for spot volume, ~12% for perp volume, and ~0% for loans outstanding. The market shares are currently at around September 2023 values, except for TVL, which is down from ~6% to ~4%.

Key Insights – The STIP’s Impact

Until now, we’ve examined how protocols within the perp DEX and spot DEX verticals have performed relative to each other within the same verticals. This offers insights into, e.g., any high-level differences in the effectiveness of different incentive mechanisms and growth themes for protocols across different maturities and sizes. However, this doesn’t allow us to say anything about the STIP’s effectiveness in maintaining or growing usage in aggregate. For example, let’s say market conditions would have drastically deteriorated during the STIP due to a systematic shock, causing all projects’ metrics to decrease throughout the program. Naively only looking at the performance of Arbitrum protocols would lead us to conclude that the program has been a failure, although what might have happened was that the total market size shrunk but the protocols’ share of the market increased, which most community members would likely objectively consider a success.

Everything else equal, it seems that the STIP successfully catalyzed a notable increase in Arbitrum’s DeFi market share across all major blockchains at the beginning of the incentive program. More specifically, it seems that ARB incentives for perp and spot DEXs, the two largest allocations, have been vast enough to meaningfully capture more of the total activity during the incentive period. However, activity began reverting in the latter half of the program, with Arbitrum’s market shares for spot volume, perp volume, and loans outstanding currently hovering around September 2023 levels. Based on the below graph, incentives were enough to sustain Arbitrum’s TVL market share at a steady level of ~6% for most of the program, but the ecosystem began losing capital relative to the rest of the market in the middle of February and currently has a ~4% market share.

Source: Artemis. Note: Major Blockchains include, where relevant, Aevo, Aptos, Avalanche C-Chain, Base, BNB Chain, Blast, dYdX, Ethereum, Fantom, Gnosis Chain, Hyperliquid, Near, Optimism, Osmosis, Polygon PoS, Scroll, Solana, StarkNet, Sui, zkSync Era

When comparing Arbitrum’s figures against Ethereum, Optimism, and Base, the trends are almost identical to those shown above, except for perp volume, which has sustained notably better. One major driver for this has likely been the successful bootstrapping of one of the newer perp DEXs on Arbitrum while protocols on the other blockchains have stagnated. This showcases Arbitrum’s strength within the perps vertical compared to the other major blockchains in the Ethereum ecosystem.

Source: Artemis

To summarize, all of the analyzed protocols saw their top-line metrics increase during the STIP, but in the months following the program’s end, figures trended back toward September 2023 values. There was some variability in how much capital/volume each protocol had managed to capture per ARB spent at the end of the STIP, but in the long term, these multiples tended to converge to a tight range. There are a few exceptions to this—protocols that are on the younger side and generally offer differentiated products. These protocols have successfully reached notably higher “steady states” compared to the beginning of the program, with incentives likely amplifying market penetration deriving from intrinsic drivers and on a few occasions, leading to more robust collaboration between the outperformers and other Arbitrum protocols, creating additional synergies. Although the data isn’t shown in this report, the money market vertical generally showcased similar trends as the perp and spot DEX verticals.

While a handful of protocols outperformed by sustainably growing activity, the overall increases in Arbitrum’s market shares across TVL and the major DeFi categories have largely reverted. In other words, the STIP doesn’t seem to have led to sustainable market capture in aggregate. However, there are other indirect returns that could be considered as well. For example:

- Incentives are an implicit avenue for the DAO to convert ARB in the treasury to ETH through the sequencer margin as activity increases during incentive programs. Although, some might argue that this isn’t the most effective way to diversify the treasury.

- If designed correctly, incentives could theoretically increase existing users’ loyalty and goodwill to Arbitrum. This is quite intangible and difficult to measure.

- Incentives might attract new builders and protocols to the ecosystem. Although this is difficult to measure in such a short time period, there are tangible examples of protocols migrating to the ecosystem with Kwenta and Curve Lending both launching on Arbitrum with onboarding incentives. However, through our conversations with several protocols, it has also become clear that the incentive application process might be too complex for many smaller teams, and some projects have decided to not even consider launching on Arbitrum as they feel like receiving funds requires too much politics.

- Intuitively, as incentives clearly increase activity, protocols benefit from earning more revenue, and it makes sense for Arbitrum protocols to also benefit as they are an integral part of the ecosystem. In contrast, the feedback we’ve received from some teams is that because meeting KPIs is such an important factor for being considered a successful STIP recipient, some projects have had to decrease their native fees to a minimum. It seems fair to say that in such cases, growth objectively isn’t sustainable, and might also hurt other protocols within the same vertical since they have to match a fee structure that isn’t profitable.

Lastly, it could be argued that had the STIP not happened, Arbitrum’s market shares across different metrics would be worse than what they are now. Such a counterfactual analysis carries many complexities and requires subjective interpretation, meaning that it isn’t possible to come to a result that can be considered the objective truth. Nevertheless, Blockworks Research has released two analyses employing the Synthetic Control causal inference method, which strives to compare what the performance of perp DEX and spot DEX STIP recipients has been during the program against what the performance would have been had the STIP not taken place.

Operational Observations

Throughout our analysis, certain wider-reaching themes and recurring developments have presented themselves, which are covered below. To begin with, incentive programs that ended notably earlier than others (i.e., February and early March) generally experienced vast capital/user outflows relative to other, similar STIP recipients when their programs ended in the latter half of March 2024. This makes sense rationally. The cost of capital within the Arbitrum ecosystem heightens during the STIP because protocols provide boosted yields and lowered fees through incentives. When one protocol stops allocating incentives, users and capital move to other protocols that are still providing heightened returns and lower expenses.

As such, allocating incentives to a concentrated group of protocols or tiering incentives across protocols within the same vertical might lead to unwanted outcomes. It’s likely that the protocols distributing incentives end up largely capturing capital and users from other projects within the ecosystem that aren’t distributing incentives, meaning that activity mostly rotates around from protocol to protocol within Arbitrum instead of bringing in new usage from foreign ecosystems.

Related to this, resulting yields across liquidity provision opportunities have had some notable variations across protocols, even within the same verticals and similar pools. Naturally, some opportunities are more risky than others because of, for example, inherently different mechanisms or less tested smart contracts, and should thus theoretically offer higher yields to reward users for taking on additional risk. Having said that, if protocols aim to minimize capturing capital and users from other similar projects within the ecosystem and instead bring in new users from foreign ecosystems, it might make sense to benchmark yields based on what similar protocols and products outside of Arbitrum are offering and apply slightly higher target yield intervals for STIP participants. As previously discussed, projects must naturally have the freedom to finetune their incentive distributions depending on, e.g., market conditions, the need to bootstrap new products, and reacting to protocol-specific needs, but especially for medium- and large-sized projects that aren’t bootstrapping new pools or products, it might be sensible to set targets.

The point here is that if similar opportunities within the ecosystem offer similar returns somewhat constantly, users within the ecosystem are disincentivized to change protocols purely based on returns. Theoretically, if growth within a vertical were to stagnate at certain yield thresholds, this implies that existing usage is exhausted at those levels and the prevalent market conditions, while the marginal new user requires higher returns to migrate to the ecosystem. In this case, it would be sensible to increase the specific vertical’s/product type’s threshold yield. Rationally, incentives shouldn’t sustainably expand existing users’ usage behavior or willingness to put capital at risk, meaning that it might make sense to add some sustainability-related KPIs to the program and more heavily prioritize structures that are likely to get new users to migrate to the ecosystem and create long-term activity.

It is worth pointing out that some standardization is already taking place, with notable perp DEX incentive recipients agreeing to rebate a maximum of 75% of trading fees. On the topic of standardization and program structure clarity, it’s exceptionally difficult to follow what the total, final number of ARB received by protocols with partnership allocations has been. Some projects have received a notably larger number of tokens compared to the initial allocation in isolation. To be specific, if partnership allocations aren’t adjusted for, comparing STIP recipients’ historical performance could lead to skewed results.

Many protocols missed several bi-weekly reports or didn’t post them at all. Around 35% of all STIP recipients didn’t post a final report. For the bi-weekly reports, only a handful of projects discussed protocol-related events and developments that might have explained growth that had materialized. Instead, it was more usual that projects would only present some high-level KPIs and how they planned to use incentives in the coming two weeks across different allocation buckets, meaning that it was sometimes difficult to understand drastic changes in figures purely based on information provided on the forum. It might be worth considering decreasing the reporting frequency to a monthly cadence, or even lower, such that protocols have more time to prepare their reports, can cover more relevant information, and hopefully can direct most of their focus on growing their products.

It was infrequent that protocols rigorously justified why they should be allocated a certain amount of incentives when applying for the STIP. Rather, the final allocations were generally a result of back-and-forth between protocols and the community, often resulting in an allocation based on something akin to “we feel like this ask is too big/small”. To make allocation requests more quantifiable and comparable across medium- and large-sized applicants, metrics such as TVL/volume/users/etc. could be normalized relative to the requested ARB allocation, creating a high-level metric that could be used to compare projects within the same verticals more easily. There are naturally additional factors that should be considered when deciding allocations as well, but multiples could be an efficient way to sanity-check protocols’ requests relative to each other.

The initially planned incentive period for the original STIP was ~3 months. This ended up being somewhat longer for Round 1 recipients, and somewhat shorter for Round 2 recipients because of the reasons mentioned at the beginning of this report. The average distribution period for relevant STIP Round 1 protocols that weren’t hacked and applied to the STIP-Bridge was 129 days, while the average distribution period for relevant STIP Round 2 protocols that weren’t hacked and applied to the STIP-Bridge was 83 days.

Some projects, even those having received incentives as part of Round 1, had a notable amount of their ARB allocations left when the STIP deadline began approaching. From a protocol’s perspective, it is naturally more beneficial to utilize as much of their incentive allocation as possible, while protocols don’t really gain anything from returning funds at the end of the period. As such, some protocols that had been more conservative in allocating ARB throughout the program arbitrarily cranked up their incentive distribution at the end of the period, which again theoretically affected the cost of capital structure within the ecosystem.

Finally, some projects that were eligible for incentives had planned to allocate ARB to products that hadn’t yet launched or to leverage incentive distribution mechanisms that hadn’t yet been put in place when the applications were submitted. Many of these projects then didn’t manage to launch the product or distribution mechanism, generally leading to the ARB allocation being redirected to some other incentive bucket instead of being sent back to the DAO. It might be sensible to require that the to-be-incentivized product has been live for X days before a protocol can request incentives for that product. Rysk has already set a great example for this, forfeiting from the STIP-Bridge since the project is currently working on its v2 upgrade. Somewhat relatedly, certain protocols built on top of another protocol’s product incentivized usage while the underlying protocol’s product was being wound down to be replaced by a newer version. Directing incentives to a product that will be discontinued in the near term might not be the highest ROI opportunity for the DAO.

Final Allocation of STIP Incentives

50M ARB was initially earmarked for the STIP. However, following higher-than-expected demand for incentives by protocols and to distribute tokens across a larger number of projects, the initial allocation (Round 1) was accompanied by a Round 2 (a.k.a. the STIP Backfund). Round 2 distributed capital to all approved but not funded projects connected to the initial allocation, amounting to ~21M ARB. In other words, a total of ~71M ARB was allocated to the overall STIP program.

Most protocols funded through Round 1 began distributing incentives in early/the middle of November 2023, while Round 2 protocols generally initiated their incentive programs at the end of December 2023 and throughout January 2024. Initially, both programs were to end by January 31, 2024, but due to backfunded protocols receiving their streams with a delay, the timelines for both programs were extended to March 29, 2024.

Source: Arbitrum Forum, Arbiscan, Blockworks Research Analysis. Note: The data excludes protocols that interrupted their distribution during the STIP, have allowed users to earn ARB rewards after March 29, 2024 (note: protocols that have allowed users to collect rewards earned during the STIP after the deadline are included), are labeled as infrastructure, and have migrated from Arbitrum. The number of ARB also excludes incentives originating from protocols’ balance sheets.

During the program, nearly all projects modified their initially proposed incentive allocations, with some even implementing completely new, unmentioned mechanisms. Modifying allocations between disclosed incentive buckets should be expected as protocols need flexibility in the way they allocate incentives as their programs progress, depending on factors such as market conditions, bootstrapping needs, and perceived effectiveness. However, it was somewhat surprising to see several protocols introduce completely new incentive buckets that were not disclosed in any way in the original incentive applications or initial bi-weekly updates.

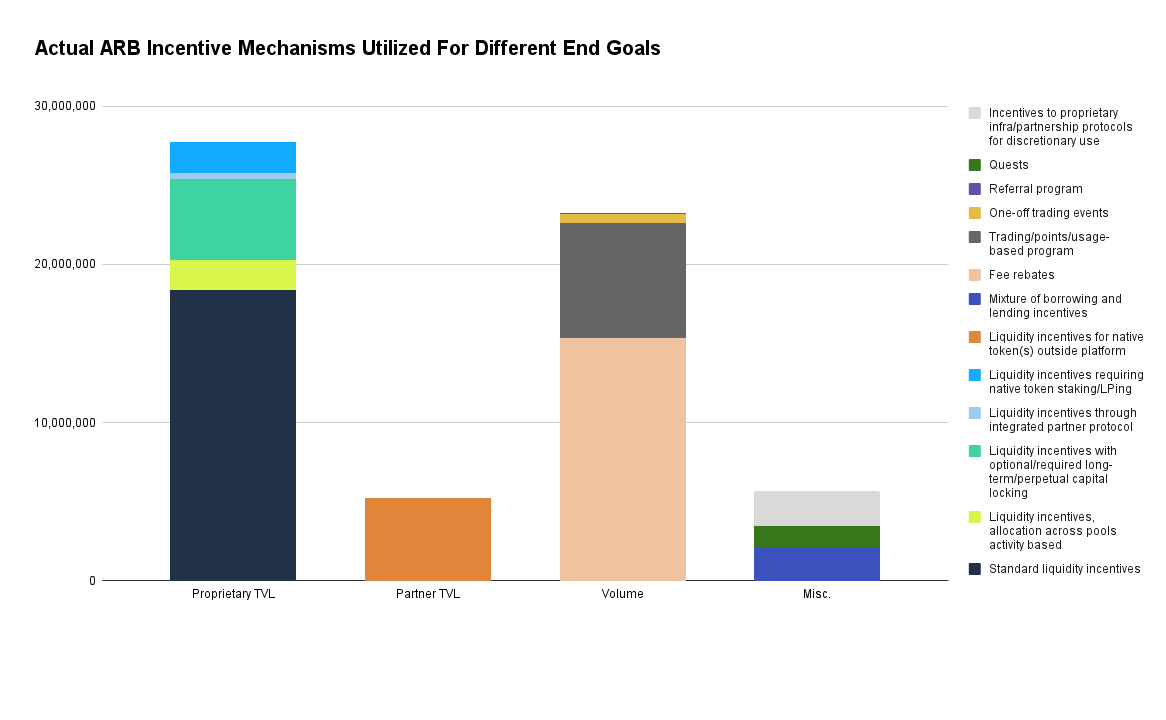

To gauge how much ARB has been utilized across different end goals, we’ve divided the distribution into four high-level groups depending on the type of user activity they primarily target. Proprietary TVL refers to incentive mechanisms that directly encouraged users to deposit liquidity into the protocol that distributed incentives. Partner TVL means that the protocol distributing incentives allocated ARB to another project’s liquidity pools. The volume category includes incentive mechanisms that directly encouraged users to move more volume through the distributing protocol’s platform.

Utilized incentive mechanisms have also been classified into different categories based on their high-level characteristics. Standard liquidity incentives refers to structures where ARB distributions and amounts across pools were decided by the protocol teams and receiving rewards didn’t require anything in addition to providing liquidity. The “Liquidity incentives, allocation across pools activity based” category is similar but the allocation structure and amounts were decided by a predetermined formula instead of being controlled by a team on a week-by-week basis. The “Liquidity incentives with optional/required long-term/perpetual capital locking” category refers to structures where users could earn more rewards by locking capital with the distributing protocol or were required to do so to be eligible for rewards. “Liquidity incentives through integrated partner protocols” means that the distributing protocol allocated liquidity incentives to another protocol, and an increase in the latter’s TVL also directly increased the allocating protocol’s TVL. “Liquidity incentives requiring native token staking/LPing” refers to a structure where a user had to acquire and either stake or LP the distributing protocols native token to be eligible for rewards. The “Liquidity incentives for native token(s) outside platform” category comprises mechanisms where distributing protocols allocated incentives to another protocol’s liquidity pools, which didn’t directly increase the distributor’s TVL. An example of this is the distributing protocol incentivizing a spot DEX’s LPs that provided liquidity for the distributor’s governance token. “Incentives to proprietary infra/partnership protocols for discretionary use” refers to mechanisms that, e.g., allocated ARB to projects to cover the costs of integrating with the distributing protocol, or allocated ARB to the distributing protocol’s partners that could freely decide how to distribute the rewards to their users.

Following the changes made throughout the STIP, the most popular mechanisms were standard liquidity incentives (~30% of total allocation), fee rebates (~25% of total allocation), trading/points/usage-based programs (~12% of total allocation), liquidity incentives for native token(s) outside platform (~8% of total allocation), and liquidity incentives with optional/required long-term/perpetual capital locking (~8% of total allocation). In aggregate, ~45% of ARB distributed was directly connected to increasing proprietary TVL, ~38% to increasing volume, ~9% to miscellaneous end goals, and ~8% to increasing partner TVL.

Source: Arbitrum Forum, Arbiscan, Blockworks Research Analysis. Note: The data excludes protocols that interrupted their distribution during the STIP, have allowed users to earn ARB rewards after March 29, 2024 (note: protocols that have allowed users to collect rewards earned during the STIP after the deadline are included), are labeled as infrastructure, and have migrated from Arbitrum. The number of ARB also excludes incentives originating from protocols’ balance sheets.

STIP Recipient Performance

We’ve chosen to focus this analysis on perp and spot DEXs as these groups were the two largest verticals to receive incentives at ~38% and ~15% of the total allocation, respectively. Moreover, it’s no secret that DeFi activity is one of Arbitrum’s main competitive strengths, with DeFi-related protocols historically accounting for over 25% of the blockchain’s sequencer revenue.

To gauge the sustainability of activity and stickiness of capital on a relative basis across different incentive mechanisms and verticals, the following sections present several normalized charts, where figures have been standardized to September 2023 beginning-of-month values. It’s important to note that it’s naturally easier for a smaller protocol to grow by, e.g., 2x, compared to a well-established protocol. However, the idea behind normalizing performance is to be able to compare how sustainable activity has been across protocols, while we have strived to analyze the relative effectiveness, impact, and perhaps fairness of the incentive distributions by normalizing absolute changes in performance metrics by ARB utilized to directly increase the relevant metrics.

The analyzed protocols are displayed in the following format: the relevant incentive mechanism(s) utilized; the size of the ARB allocation received (where Small: < 1M ARB; Medium: >= 1M ARB & <= 2M ARB; Large > 2M ARB); the round through which incentives were received. To not distort this analysis, we’ve only considered protocols that have distributed incentives continuously for over two months, haven’t been hacked since the beginning of September 2023, and have been operational before the beginning of September 2023. A few protocols were also excluded due to reliable performance data not being readily available.

Perp DEXs

TVL

Source: DefiLlama & Dune

Within the perp DEX vertical, one protocol outperformed others when looking at normalized TVL figures. This protocol is on the younger side compared to the peer group, and as mentioned earlier, it’s naturally easier to reach large relative growth numbers when initial figures are smaller. That is not to say that the result isn’t impressive, especially given that the TVL growth continued after the program ended and has now essentially stabilized. However, this growth has most likely mainly been driven by factors intrinsically connected to the protocol, such as finding product-market fit, business development efforts, native liquidity incentives, bootstrapping market makers, etc. Nevertheless, we consider this as a great example of where incentives can be beneficial, with ARB tokens likely having amplified growth, which the protocol has managed to maintain post-STIP incentives. One possible downside to consider is that some capital might have migrated from other Arbitrum-aligned perp DEXs but increased competition on the supply side is in general beneficial for end users.

Source: DefiLlama & Dune

TVL development for the rest of the protocols within the perp DEX vertical follows a somewhat unified pattern. In general, liquidity began increasing around the time each protocol’s incentive program commenced, remained elevated during the program, but started decreasing as incentives drew to an end. It also seems that Round 2 protocols have been at a disadvantage, with liquidity trending downward until their incentive programs were initiated.

For half of the group, liquidity has dropped notably below levels where it was when the incentive program began, while for the other half, liquidity is slightly higher than what it was when the programs were initiated. Theoretically, each protocol has a baseline liquidity level that it can attract, depending on yields offered, perceived riskiness of returns, as well as LPs’ opportunity cost. On a high level, yields go down when incentives end since some trading volume is bound to migrate and immediate ARB rewards to LPs taper, inducing some LPs to move to other sources of yield that they perceive to be better.

Interestingly, the two protocols that used ARB to directly incentivize LPing on their platforms didn’t see as drastic drawdowns in their TVLs as experienced by the two protocols that used no incentives for proprietary TVL. Another factor to consider is that market conditions drastically improved during the STIP and asset prices shot up. The impact of this on perp DEXs depends on the protocol design, as some perp DEXs mainly rely on stablecoins for liquidity, while others’ TVLs consist mostly of volatile crypto assets. In ETH terms, every perp DEXs’ TVL is down on a normalized basis, excluding the outperformer mentioned earlier.

Source: DefiLlama, CoinGecko, Dune

Source: DefiLlama, CoinGecko, Dune

Three of the five perp DEXs analyzed used incentives to directly increase proprietary liquidity. Looking at TVL figures at the beginning of September 2023 normalized by ARB allocated for increasing proprietary liquidity throughout the program shows that there was some notable variation in how much ARB was used as liquidity incentives relative to TVL levels. If liquidity was purely driven by direct ARB incentives, projects with smaller TVL / ARB incentives allocated starting multiples should see their multiples expand more throughout the program than projects with large starting multiples.

Source: DefiLlama, Arbitrum Forum, Arbiscan, Blockworks Research Analysis

The best performer reached ~$135 additional 30D-MA liquidity compared to the beginning of its incentive program per ARB spent. TVL continued climbing after the program ended until the middle of April, and the metric stabilized at ~175$ at the end of June 2024. Excluding the best performer leaves a small sample size, but the long-term TVL growth per ARB spent across the other two protocols is quite similar despite the fact that one utilized notably larger liquidity incentives relative to its TVL than the other, and the utilized incentive mechanisms were quite different. This might indicate that as long as teams allocate incentives sensibly, the underlying mechanism doesn’t significantly matter since the return LPs require is similar across protocols. Simply put, opportunities with similar risk profiles should also have similar costs of capital.

Source: DefiLlama, Arbitrum Forum, Arbiscan, Blockworks Research Analysis

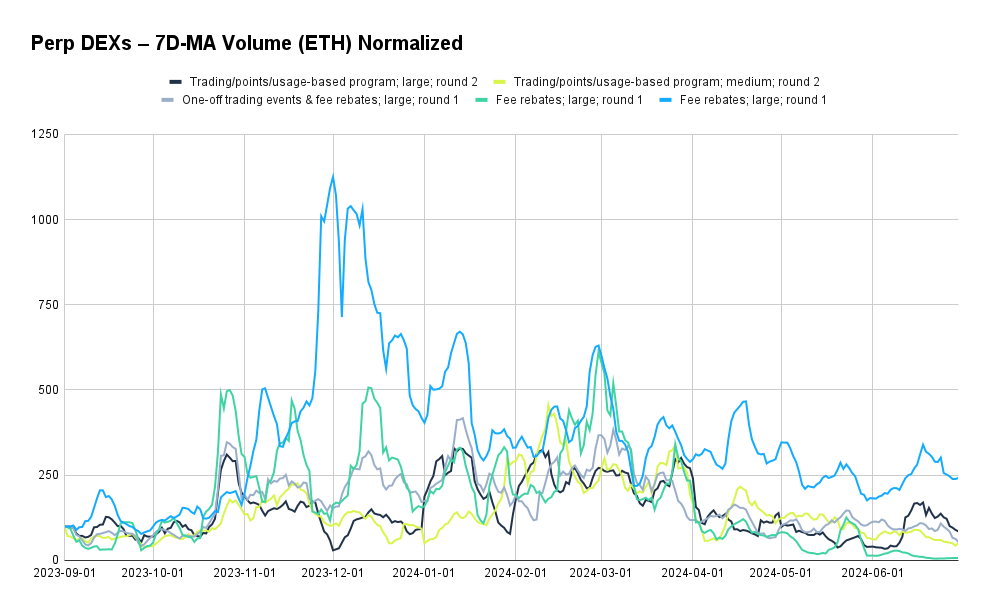

Volume

The volume trends for perp DEX STIP recipients follow the TVL trends quite closely, where the same outperformer managed to grow during its incentive program as well as maintain the increased activity after the program ended. Meanwhile, the rest of the protocols experienced notable uptrends in volume coinciding with the beginning of their incentive programs, but this trend began reverting in early April, converging towards September 2023 values in June 2024. Similarly to TVL, round 2 recipients’ figures lagged behind round 1 recipients’ but began catching up in the latter half of the STIP.

Source: DefiLlama & Dune

Source: DefiLlama, CoinGecko, Dune

The outperformer utilized the least ARB to directly incentivize trading volume relative to volume at the beginning of September 2023, at 1 ARB per ~$21 of volume. This indicates that the outperformance in growth didn’t derive from an outsized allocation of incentives relative to volume when compared against other perp DEXs. For the rest of the perp DEXs, there is some spread in the Volume / ARB utilized multiple, ranging between $6-$12.

Source: DefiLlama, Dune, Arbitrum Forum, Arbiscan, Blockworks Research Analysis

Source: DefiLlama, Dune, Arbitrum Forum, Arbiscan, Blockworks Research Analysis

As with TVL, there is some variability across absolute volume growth achieved at the end of the STIP per ARB directly used to incentivize activity, with increases for the incentive periods ranging between ~$10 and ~$39, excluding the outperformer which achieved volume growth of ~$93 per ARB spent. However, these figures began converging in the months following the STIP’s conclusion. At the end of June 2024, the absolute changes in volume compared to the beginning of each perp DEX’s incentive program per ARB spent were ~$6, ~$1, ~-$2, and ~-$21, excluding the outperformer, for which the figure was at ~$55. In other words, projects have generally achieved similar returns when looking at a longer time period.

Source: DefiLlama, Dune, Arbitrum Forum, Arbiscan, Blockworks Research Analysis

Spot DEXs

TVL

Within the spot DEX vertical, there was one outperformer in terms of relative TVL growth, and this growth has sustained post-incentives. Similarly to the outperformer within the perp DEX vertical, this protocol is on the smaller/younger side, meaning that only looking at relative growth can be misleading. Nevertheless, incentives have facilitated the protocol to achieve a sustainable market share increase, although this is unlikely to be the main driver for outperformance.

For the rest of the protocols, all of which are Round 1 recipients, relative TVL growth moved in tandem until the end of March 2024, when one perp DEX lost notably more liquidity compared to the rest of the group. This protocol is the only spot DEX that had a lower TVL at the end of June 2024 compared to the beginning of September 2023. Compared to perp DEXs, this vertical’s USD-denominated TVL is even more heavily driven by volatile crypto asset prices. As crypto prices generally increased in Q4 ‘23 and Q1 ‘24, USD-denominated TVL would have increased even with no asset inflows to spot DEXs. Looking at TVL denominated in ETH, only the outperformer’s figures are up from September 2023 values.

Source: DefiLlama & Token Terminal

Source: DefiLlama, CoinGecko, Token Terminal

All of the analyzed spot DEXs used all of their incentives to directly increase proprietary liquidity. The below two graphs are great examples of why it’s helpful to normalize high-level metrics by the ARB allocation size. As mentioned earlier, one spot DEX outperformed when it comes to relative TVL growth. However, the same protocol also received the largest ARB allocation relative to its TVL at the beginning of September 2023, with one ARB allocated per ~$4 of liquidity. In comparison, the other spot DEXs received one ARB per liquidity between ~$19-~$71.

Source: DefiLlama, Token Terminal, Arbitrum Forum, Arbiscan, Blockworks Research Analysis

Performance relative to the allocation size varied widely between protocols at the end of the STIP, with Round 1 recipients having reached notably stronger results. However, three months later, all except for one protocol’s figures had converged to similar levels at ~$13, ~$17, and ~$20, while the underperformer was at ~-$25. In other words, the long-term benefit of one ARB spent has been quite similar across most spot DEXs. It’s worth noting that the underperformer utilized a predetermined formula that was based on other factors than just fees generated across pools, which might have been gameable and attracted mercenary capital, possibly explaining the drastic drawdown once the STIP ended. However, this isn’t something that we can say to be objectively true just based on the data presented. Nevertheless, in contrast, the other spot DEX that allocated LP incentives based on a predetermined formula did so purely based on fees generated. The below graph also exemplifies why purely examining growth figures achieved during the incentive program could be misleading. While one spot DEX outperformed when looking at values from the end of March, its TVL performance per ARB spent has actually been the weakest in the long term.

Source: DefiLlama, Token Terminal, Arbitrum Forum, Arbiscan, Blockworks Research Analysis

Volume

As mentioned earlier, no spot DEXs directly incentivized traders with ARB. Despite this, all protocols’ volume figures grew notably during the program, with two projects having outperformed and largely maintained volume after the program ended. The two other protocols also saw a clear uplift in volume during the program, generally coinciding with wider market trends, but the drawdown post-STIP has been more drastic on a relative basis than for the two outperformers, both of which are newer protocols. It should be noted that the active liquidity management protocol Gamma was exploited on January 4, 2024, which led to abnormally high volumes on that day for a few protocols analyzed here.

Source: DefiLlama, Token Terminal

Source: DefiLlama, Token Terminal

Again, market conditions in Q4 ‘23 and Q1 ‘24 were favorable for perp DEX volume, and relative growth should be expected for all projects when looking at USD-denominated values. Having said that, instead of simply benefitting from increased asset prices and more volatility, the two outperformers have likely grown by also increasing their market penetration, exceeding the market’s expansion. Looking at ETH-denominated volume, the two outperformers have largely maintained their relative growth, while volume for the two other projects has returned to September 2023 levels.

Source: DefiLlama, CoinGecko, Token Terminal

Source: DefiLlama, CoinGecko, Token Terminal